The purchase of a property may be the largest investment a consumer makes in his or her lifetime; it could also be business as usual for a large investment company. Either way, an integral part of that transaction is assessing for and protecting against risk – both of which are addressed by securing title insurance.

Historical Problems

Prior to the institution of title insurance, purchasing real estate in the United States was a far riskier venture. During a property transaction, conveyancers would establish the rights of title to a property based on public records searches or other property abstracts. The title would necessarily be cleared of any liens, rights or other encumbrances prior to conveying the property to new buyers or lending against the property; however, with limited resources and no insurance backing, the risk of losing a property due to unresolved issues was still significant. Additionally, if an unresolved issue caused problems, the harmed borrower or lender would have to prove legal negligence in order to collect damages from the conveyancer for his or her errors, which can be difficult.

Watson v. Muirhead

Although it now protects land purchases across the United States (as well as other areas of the globe), the practice of insuring title began after a Pennsylvania Supreme Court ruling in 1868. The case, Watson v. Muirhead, 57 Pa. 161, settled the matter of ownership over a property purchased after an “abstract of title,” or title records search, was conducted. During his research, the transaction conveyancer found a lien on the title, which he then turned over to an attorney for legal opinion. The attorney advised that the judgment was not in fact a valid lien. With this assurance, the conveyancer and purchaser completed the transaction.

Not long afterward, the property was sold at a Sherriff’s sale in order to pay off the lien, which was in fact lawful.

The court ruled that the lien, and thus the Sherriff’s sale, was indeed lawful, and the conveyancer involved in the transaction was not held liable for misinformation because the legal standard was “negligence,” or failure to act with due care. Since the conveyancer had relied upon an attorney’s opinion that the lien was invalid, the conveyancer had used due care — even if he was incorrect.

The First Title Insurance Company

The judgment, and subsequent loss to the purchaser, then prompted a group of Philadelphia conveyancers to establish a way to protect the innocent buyers of real property. In 1876, this group formed the first title insurance company, whose mission it was to protect “the purchasers of real estate and mortgages against losses from defective title, liens and encumbrances,” and added, “through these facilities, transfer of real estate and real estate securities can be made more speedily and with greater security than heretofore.”

Shortly thereafter, title insurance companies became established in other large metros throughout the United States, including New York City, Chicago, Minneapolis, San Francisco and Los Angeles.

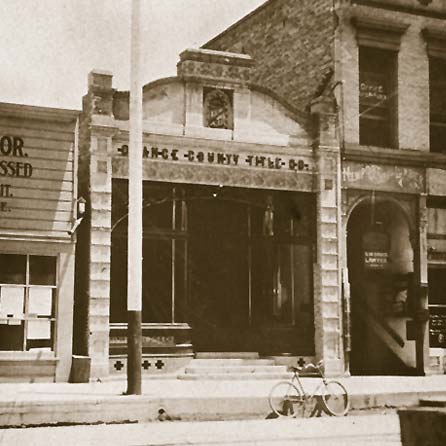

The Birth of First American

In 1889, just over 20 years after the birth of title insurance in the United States, the Orange County Title Company was established; the original predecessor to First American Title Insurance Company.